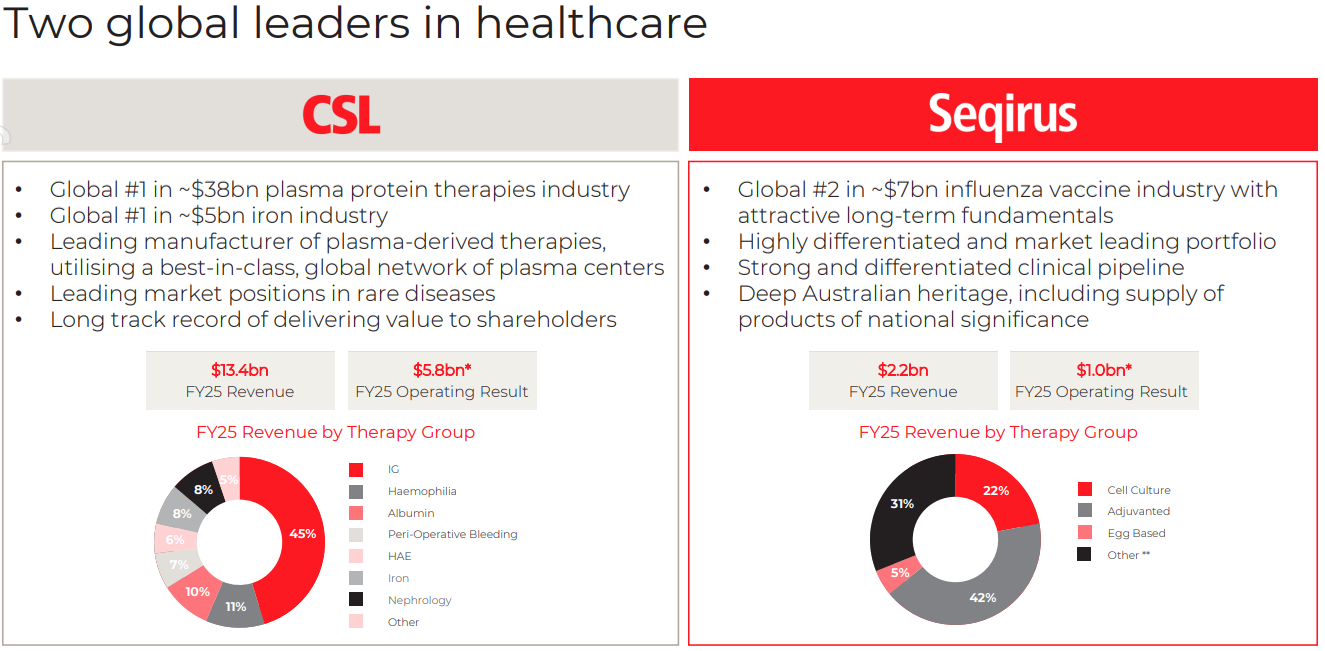

CSL (CSL) reported its full-year 2025 profit results, which came in with mixed results, with a stronger Plasma and Iron division offsetting weakness in the Vaccines division. The intention to spin out the vaccines business and a significant reduction in headcount to cut costs came as a surprise to the market. The HNW Core Portfolio holds an 8% weighting to CSL.

Key Points:

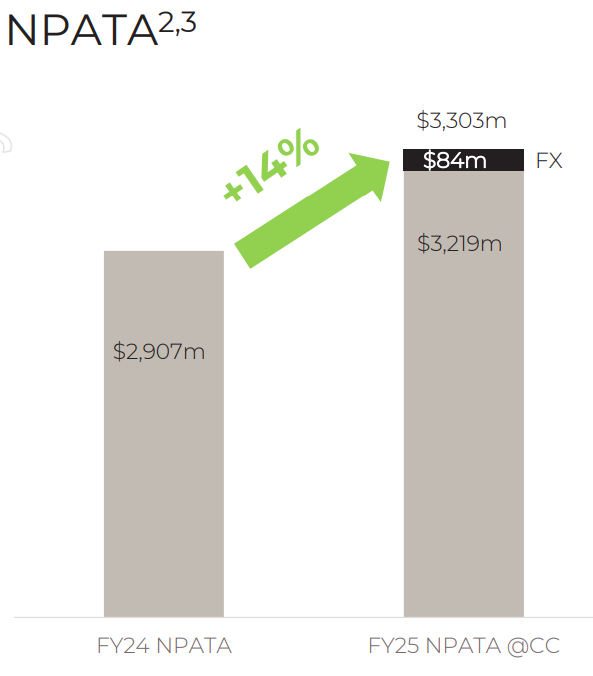

- Record Profits: CSL profits were up +14% to $3.3 billion, driven by a strong year from their Behring business and from their Vifor Iron Deficiency division, which saw revenue increase by 8%. CSL’s vaccine division reported a 2% increase in revenue to $2.1 billion, following a soft vaccination period in the US earlier this year, as consumers experienced vaccine fatigue due to the pandemic.

- Cost outs to Come: CSL is planning to save US$500 million annually, driven by a 15% reduction in headcount due to the increase in labour following the Covid surge. This will result in 22 plasma centres in the US being closed, and the manufacturing footprint will decrease from 11 sites to 6.

- Spinning out Seqirus (Vaccines): CSL management has announced that it will demerge its Seqirus (Vaccines) Division to create a new Top 100 ASX-listed company. Whilst vaccines fall under the healthcare banner alongside blood therapy and iron deficiency, they have fundamentally different business models, selling to governments for disease and pandemic prevention as opposed to selling to patients and doctors for life-saving treatments. The demerger will also create a narrower focus for the R&D divisions and a more effective capital allocation across the business.

- Dividend: +12% to A$4.50 per share, representing a payout ratio of 44% as CSL continues to expense its R&D spend through the P&L rather than on the balance sheet, the much cleaner option in the Atlas opinion.

- On-Market Share Buyback: CSL management announced a $750 million buyback, citing strong cash flows over the last 12 months. Management outlined that the size of the buyback is likely to increase over the medium term.

- Guidance: CSL management reiterated their full-year guidance of 4-5% revenue growth and 7-10% profit growth for 2026 and beyond, with strong expectations from Behring and Vifor over the medium term. EPS could be higher with share buy-backs.

- Why is the stock down? CSL is down today due to concerns about revenue growth in the early 2030s, following the failure to obtain approval for CSL-112 and other smaller R&D projects. Following the spin-out of Seqirus, more focus will be placed on R&D, as well as profitable growth, rather than growth at any cost. As investors, we are concerned with profits and dividends, not revenue, as revenue growth means little if it is not profitable.

Portfolio Strategy: CSL is a world leader in manufacturing medicines from human blood and flu vaccines, and, along with Sonic Health, is a core healthcare position in the Portfolio. The business enjoys substantial barriers to entry, with stable margins, and, in Australia, holds exclusive rights to the production of blood plasma-derived medicines. The company earns over 90% of its profits offshore and benefits from a falling AUD. Key catalysts over the next 12 months will be the commencement of the on-market share buyback and the demerger of the vaccine business, which will create a more streamlined and higher-margin business.

CSL finished down -16.9% to $225.50, a savage reaction to management guiding to earnings growth in 2026 lower than market expectations , but reflects the volume of corporate changes that management released today.