Charter Hall Retail (CQR): This morning, the supermarket landlord reported their full-year results for 2025, which were largely in line with market expectations. Though generally, there should be minimal excitement on results day for this very boring and stable supermarket trust. HNW Income has an 3.75% weighting to CQR.

Key Points:

- Earnings Down: CQR reported operating earnings of $148 million, down 7%, driven primarily by an increase in interest costs and repayments, alongside $158 million in divestments. This was partially offset by a 2.7% increase in rental income.

- Balance Sheet: Following the increased ownership of HPI during the year, CQR’s gearing stands at 27%, with an average cost of debt of 5% and an average debt maturity of 3 years.

- Distribution Flat: CQR reported the full-year distribution of 24.7 cents per share, in line with last year’s distribution.

- Valuation: NTA increased by 13 cents to $4.64, following convenience retail valuation growth driven by inflation-linked rental income.

- Outlook: CQR management guided for FY26 operating earnings to be $0.26 per unit, with a distribution of $0.25 per unit, representing a 3.5% increase in this year’s distribution and a 6.5% distribution yield.

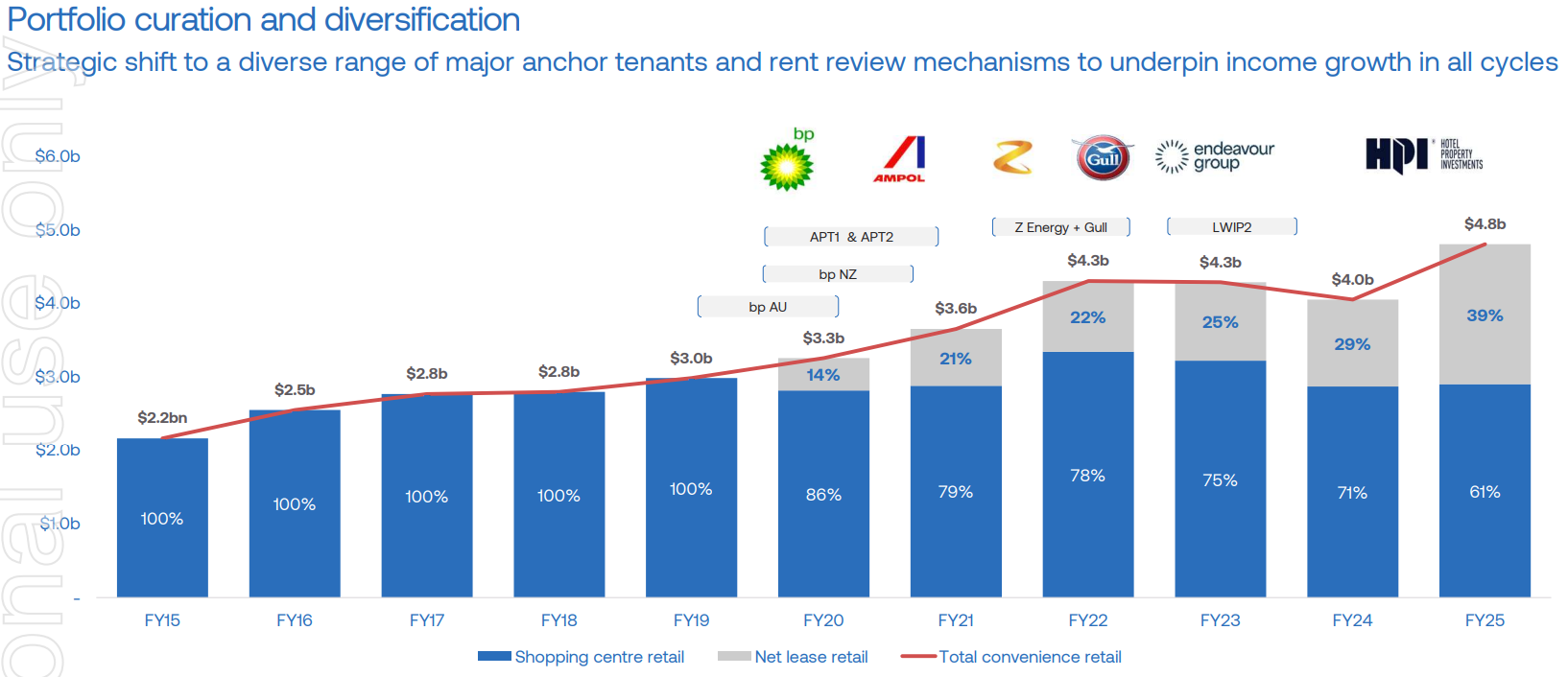

Portfolio Strategy: CQR offers portfolio exposure to non-discretionary retailing through a diversified portfolio of neighbourhood shopping centres, typically anchored by a Woolworths or Coles supermarket, as well as service stations. Long leases linked to the CPI, such as those with quality tenants like Woolworths, Coles, Aldi, and BP, provide a high degree of confidence that CQR can maintain and grow its distributions over time.

CQR finished down 0.5% to $4.06 – a 12.5% discount to NTA.