Lendlease (LLC), the formerly multinational construction and asset management company, reported its half-year results for 2026, which showed that the turnaround plan still has a way to go. The HNW Core Portfolio holds a 1% weight to LLC, the smallest position in the portfolio.

Key Points:

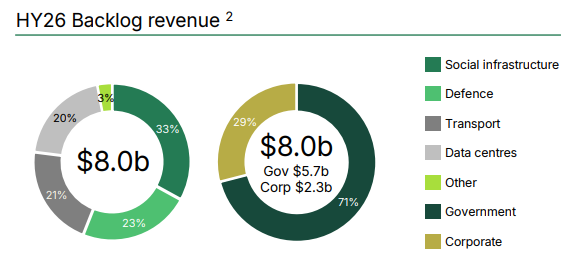

- Profits Down: Lendlease profits were down to an operating loss of $200 million, driven primarily by non-cash impairments and lower valuation of assets held for sale. The highlight of the result was the increase in construction earnings driven by new data centre starts. This was offset by lower earnings from investments and developments due to lower sales of finished apartments.

- Shrinking to Improve: Starting last year, LLC has announced $3 billion of capital recycling initiatives, exiting international construction, US military housing, and Australian project housing. Due to the timing of the transactions, cash will not flow into the balance sheet until the first half of next year.

- Dividends Up: The LLC’s dividend of 6.2 cents per share was up 3% from last year, representing a payout ratio of 50%. The dividends are expected to increase once the cash proceeds from sales come through in the first half of 2026.

- Outlook: LLC management did not provide any guidance for next year but did say that they are targeting $2 billion in capital recycling over the next year from the sale of assets to reduce the level of debt.

- Why is the Stock down? The stock is down following the pushed-out timeline for payments from sold assets in combination with both the CEO and CFO finishing their tenor at Lendlease before completing the turnaround.

Portfolio Strategy: The market remains sceptical towards LLC after it revealed in May 2024 that its sprawling, glamorous developments in the USA and Europe had been consistently unprofitable and propped up by the company’s operations in Australia and Asia. This infuriated shareholders. Streaming some of the trapped capital out to shareholders (current $3.19 per share) will improve sentiment towards the company. While we can see the moves and asset sales made by management over the past year, scepticism will remain until investors see the colour of LLC’s money.

Atlas is currently reviewing its position in LLC, with management pushing out the timing of the tax-effective capital returns that we expected would be announced at this result. While LLC looks cheap trading on a PE of 12x, we are wary of further management change.

LLC finished down 7% to $4.25.