This morning, Ampol (ALD), Australia’s largest energy distributor and retailer, released its full-year results for 2025, demonstrating the strength of recent refining margins and the ongoing success of convenience retailing. The HNW Core Portfolio has a 3.6% weight to ALD, with the HNW Income at 5%.

Key Points:

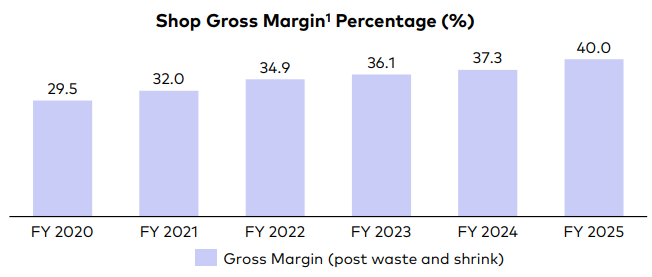

- Profits Up: Ampol’s full-year profits increased by 83% to $429 million following a return to higher margins for the refining business and the strong and stable returns from the retail business. The strong retail earnings were driven by increased margins on Powerades, Cokes, and snacks within the stores (See Below).

- Lytton Refinery: The Lytton refinery had a stronger year following an appreciation in refinery margin due to ongoing geopolitical events in the Middle East. Over the next year, the refinery will go through an ultra-low sulphides upgrade, which will increase margins even further over the next 12 months.

- EG Acquisition: Ampol is expecting to acquire EG Australia in the first half of 2026, pending approval from the ACCC. EG Australia has 500 sites, with the majority located in the eastern states of Australia. Approximately 125 sites are slated for conversion into U-GO sites, Ampol’s unmanned service offering, which has seen a $280K profit uplift per site on the 46 sites already converted.

- Balance Sheet: The Ampol balance sheet remains quite strong with net debt of $2.9 billion or 2.3x leverage, within the target leverage range of 2-2.5x. Ampol will naturally fall within the target range once Lytton’s refining margin returns before elevating post-EG acquisition again. Atlas looks at this as the preferred method for the transaction over an aggressive capital raise.

- Dividend Up: ALD announced a fully franked 100 cents per share dividend, representing a lower payout ratio of 56% of profits (target 50-70%). The dividend and payout ratio are expected to increase in the next year, as refining operating margins return.

- Outlook: Ampol management did not provide explicit guidance but did say that they are seeing higher in-store margins and stable fuel volumes across their sites in January.

Portfolio Strategy: ALD is the core energy exposure in the Portfolio, but with greater exposure to fuel and food retailing rather than the vagaries of the oil price. Over the past five years, ALD has changed from a capital-intensive business with volatile earnings dependent on global refining margins to one increasingly based on fuel and convenience retailing and bringing franchised service stations in-house. ALD trades on an undemanding = 15x forward earnings with a 5% fully franked dividend yield.

While EV penetration is increasing in Australia, in 2025, this represented only 8% of new car sales and 1% of the passenger fleet. Australian fuel demand has continued to grow, though ALD have made moves to capture revenue from EVs by installing fast chargers at 290 sites across Australasia, charging customers ~$50 to charge a Tesla while selling high-margin cans of Coke and ice blocks.

ALD finished down -2% to $28.36