Sonic Healthcare (SHL). This morning global pathology company SHL reported their full year of 2023 profit results, which came in below market expectations. These were an eagerly awaited set of results and the first to show a slowing down of PCR testing, which has offered rivers of gold for SHL. The HNW Core Portfolio has a 2.5% weight to Sonic.

Key Points:

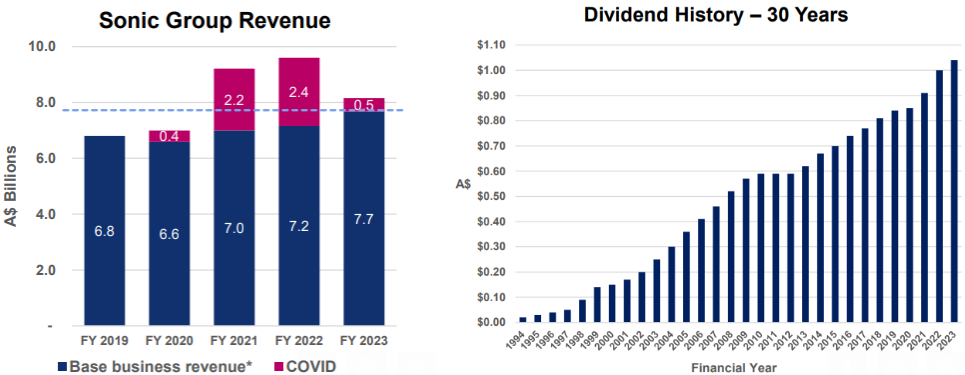

- Profits down: Full-year profits were down 53% to $685 million, as the high margin Covid testing revenue fell from $2.4 billion to $485 million. SHL provided rivers of gold for SHL, which they have used to improve the company, pay off debt and expand the business mainly in Germany, Switzerland and the USA.

- Base Business Up: What was pleasing to see was the base pathology testing business performing well, with revenue growing 11% to $7.7 billion and is now 25% ahead of where the company was pre-Covid. This was supported by strong growth in Australia, US and radiology, with acquisitions occurring throughout the year in Germany and Switzerland, further boosting Sonic’s place as a global pathology player.

- Dividend: A modest increase of +4% to $1.04 per share in line with SHL’s progressive dividend policy with a payout ratio of 71%. Franking jumps at 100% due to higher Australian profits and a low payout ratio. SHL has an excellent long-term record of rewarding shareholders (see below).

- Continued Balance Sheet Strength: Gearing at less than 10% with interest cover at 29. Over the year, Sonic bought back $425 million in stock on market.

- Why is the stock down? The market overestimated the amount of Covid-related earnings the business would be able to hold onto outside of the pandemic, with Covid-related revenue falling by 80%. As mentioned above, this should not have been a big surprise.

- Outlook: SHL provided guidance around their FY24 EBITDA range of $1.7-1.8 billion, reflecting a 5% increase of FY23 with the base business performance offsetting material reduction in COVID-related earnings.

Portfolio Strategy:

Sonic and CSL represent the core healthcare positions in the Portfolio. SHL exposes us to rising demand for medical testing, exacerbated by new medical technologies, an aging population and a desire by doctors to cover themselves against malpractice claims by increasing the number of tests being ordered. SHL is one of the largest global patient testing companies with a #1 market share in Australia, Germany & Switzerland, #2 in the UK and #3 in the USA and will benefit from a falling AUD. Unlike drug companies or device companies such as Cochlear, SHL has an industrial process of blood and tissue sample testing that benefits from economies of scale and not the hundreds of millions of dollars invested in R&D to develop the next wonder drug device.

In the medium term, SHL will benefit from an older and sicker population post-Covid and doctors scheduling more tests to avoid malpractice suits, particularly in the USA, where SHL is now the third largest pathology company.

SHL finished down -5.7% to $32.03, though despite this fall, SHL has been a solid citizen in the Portfolio +8.3% vs ASX 200 +4%.