Region Group (RGN): This morning, Australia’s biggest convenience mall landlord, RGN, released their full year 2024; the company’s results were largely in line with expectations. The HNW Portfolios have a 2% weight to RGN.

Key Points:

- Profits Lower: down -7% to $193 million due to increased interest expense and lost income from asset sales offsetting +3% property income growth. Over the past year RGN has sold $177M of non-core properties to reduce debt. The key points from the result were stabilised property valuations with no change to the 6.07% cap rate = NTA $2.42.

- Funds Management : we were pleased to see the further expansion of RGN’s funds management business with the establishment of A $394m Metro Fund, with Singapore’s GIC providing the funding & RGN managing the assets.

- Operational Performance: RGN continues to manage its portfolio well, with occupancy at 98% and a solid average lease term of 5 years. Tenant sales in the centres remained strong, with sales increasing by 2.5%, pharmacy/healthcare (+8%), medical/beauty (5%) and Supermarkets (+3%), Kmart/Big W (-2%) was weaker along with discretionary speciality (-4%). Currently, 50 anchors, or 47% of anchors, are paying turnover rent in addition to base rent, up from 31 anchors three years ago and contributed an additional $6.7 million in profit.

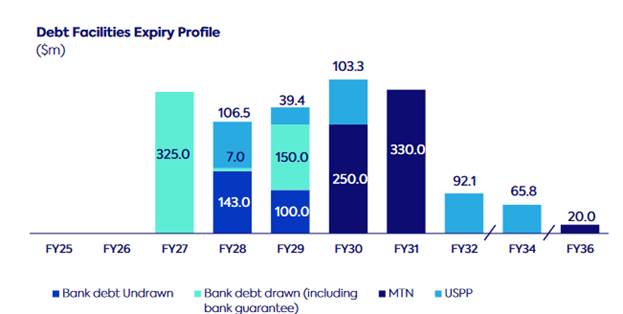

- Balance Sheet: Gearing is currently at 33%, at the low end of the target range of 30-40%. RGN saw an increase in the average debt cost to 4.4%, an average debt maturity of 4.0 years, and no debt expires until 2027. Pleasingly, RGN now has over 96% of its debt hedged or at a fixed rate.

- Guidance: RGN management have given guidance of modest growth for FY24 and DPS of 13.7 cents per share = 6% yield. Management are expecting stronger sales in FY25 thanks to the income tax cuts kicking off 1st July. Given the lower socio-economic cohort patronising RGN’s assets, previous stimulus measures had translated into higher tenant revenue.

RGN finished up 1c at $2.26.

Portfolio Strategy: RGN offers the portfolio exposure to non-discretionary retailing via a diversified portfolio of neighbourhood shopping centres typically anchored by a Woolworths or Coles supermarket with an accompanying Dan Murphy’s or BWS. The company owns 93 supermarket centres anchored by Woolworths, Coles and Aldi valued at $4.3 billion located across Australia. Unlike better-known retail landlords such as Scentre or Stockland, RGN’s tenants are not particularly exposed to the impact of online sales or falling discretionary retail spend, with consumer staples and alcohol, as well as medical and personal services such as haircuts are not easily delivered online and largely non-discretionary.

Long leases to quality tenants such as Woolworths, Coles and Aldi give a high degree of confidence that RGN can maintain and grow their distributions over time with rental income growing annually.