This morning, JB HI-FI (JBH), the local electronics and home appliance retailer, delivered a strong set of full-year results in line with expectations, which highlighted JB Hi-Fi’s strong earnings and continued market share gains. The HNW Portfolios have a 2% weight to JB Hi-Fi.

Key Points:

- Profits Up: JB Hi-Fi reported strong earnings growth of +9% to $476 million, driven primarily by a 10% increase in sales to $10.5 billion. JB Hi-Fi Australia remains the largest winner, with earnings up 8% following increased sales of AI-enhanced devices and the launch of the Nintendo Switch 2. On the call, management said that they were yet to see any benefits from suppliers impacted by Trump’s tariffs, which would make Australian retailers a more attractive customer for Chinese and Japanese manufacturers than their US counterparts

- No Debt: JBH continues to have one of the best balance sheets on the ASX, with a net positive cash position of $284 million.

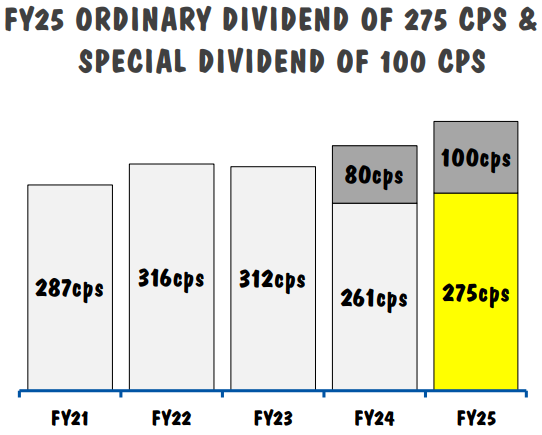

- Special Dividend: In addition to the full-year dividend of $2.75 per share, which was fully franked, JBH also announced a special dividend of $ 1.00 per share, which was fully franked, following the business’s strong capital position. (See Below) These dividends represent a 10% increase on last year’s dividend. In the future, JBH are looking to increase their payout ratio from 65% to 80% to reduce cash building on the balance sheet.

- Handing over the baton: Some in the market did not like the news of well-respected CEO Terry Smart’s retirement in October for the second time as CEO of JBH – he had initially retired in 2014 after 14 years at JBH, but was lured back in 2017. The incoming CEO is the current chief operating officer, a safe pair of hands who has been with the company since 2009, including 10 years as the CFO.

- Outlook: JB Hi-Fi management provided a strong trading update, showing that JB Hi-Fi Australia’s sales grew by over 6% in July, with The Good Guys also experiencing a sales increase of over 4% for the same month. Given JBH is cycling some tough comps from July 2024, this is a good outcome.

- Why is the stock down? Similar to QBE last week, JBH’s share price is weaker today, despite a solid result, as the market questions whether earnings have peaked. Over the past year, Atlas has reduced its JB Hi-Fi position multiple times to the minimum position size of 2% on valuation grounds. We remain attracted to JBH’s business model, which is characterised by being the lowest-cost operator, and its history of rewarding shareholders.

JBH finished down 8% to $107.83, despite this fall, JBH has been a solid citizen in the portfolio over the past year, up +65%.

Portfolio Strategy: JBH’s business model is based on low prices, low overheads, and high volumes. Regarding the cost of doing business (rent, administration and sales staff costs), divided by sales – JBH is one of the most efficient retailers globally, a remarkable outcome given Australia’s high wages and is Australia’s largest electrical retailer and the world’s seventh-largest electrical retailer.

More importantly, JBH has consistently recognised declining (CDs) and growing (fitness devices) categories and switched inventory to take advantage of these shifts; the expansion into Home and white goods has proved very successful.

While we are unhappy about today’s share price move, there is nothing in this result that changes our investment thesis. JBH remains one of the best retailers in the country and this result indicates to us that the company is increasing its market share probably at the expense of Harvey Norman (yet to report).