This morning, Dalrymple Bay Infrastructure (DBI), the world’s largest met coal export terminal, reported its first half 2026 results, which demonstrated strong earnings and distributions. The HNW Core Portfolio has a 2.5% allocation to DBI.

Key Points:

- Record Profits: DBI’s full-year profits increased by 11% to $173 million, driven by 4% increase in tolling charges for the terminal with no increases in costs, leading to 96% profit margin. DBI also benefitted from a lower interest rate environment.

- Organic Growth Coming: For every dollar that DBI invests into its terminal, they get to increase the tolling charge of the terminal. As the coal miners are the operators of the terminal, they want to invest as much as possible into the terminal to increase efficiency. Due to DBI investments over the past 4 years, tolling charges will increase by $0.70 per tonne or $59 million per year in 2027, with no increase in associated costs meaning the increased revenue goes straight to the bottom line for shareholders.

- Stronger Balance Sheet: DBI announced in December last year that it has refinanced $1.07 billion of debt at a 4.6% interest rate and termed out the length of the loan. This is a great result as the previous debt was at an 6.5% interest rate expiring next year. This move will save DBI over $75 million in interest repayments over the next three years.

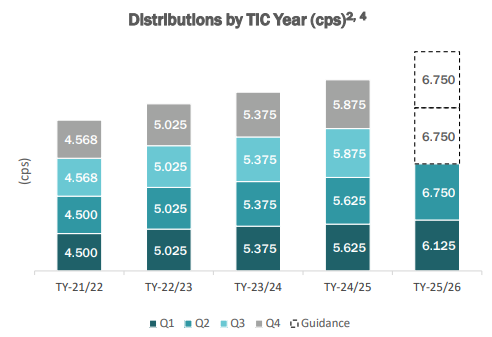

- Record Dividend: DBI announced a full-year dividend of 24.6 cents per share, representing 11% growth on last year’s dividend.

- Outlook: DBI management did not provide explicit guidance but did announce that they expect dividends for the next two quarters to total 13.5 cents per share (See Below).

Portfolio Strategy: Dalrymple Bay Infrastructure is the concession holder of the world’s largest met coal export terminal. We are attracted to DBI due to its high quality, long life, and largely monopolistic infrastructure asset. The company has demonstrated an ability to grow distributions ahead of inflation by both raising the tolling charge and organic development of its asset. DBI revenues are independent of commodity prices and are linked to CPI and development returns, and trades on an attractive 5% dividend yield.

DBI finished up +6.5% to $5.45, DBI has performed well since adding it to the Portfolio in September last year.