Amcor (AMC) Last night, the world’s largest consumer packaging company announced its results for the full year of 2025, which included two months of operations from the newly merged Berry business. As expected, this was a difficult result to analyse, given the number of moving parts involved in consummating a very large acquisition. The HNW Portfolio has a 4.5% weight to AMC.

Key Points:

- Profits Lower: Full year profits up +13% to US$1,136 million with earnings per share up only 3% to US$0.71 due to the full impact of increased shares issued to acquire Berry and only two months of additional profits. In flexibles, lower demand in the USA was offset by growth in LatAm and Asia, with the segment generally benefiting from a favourable product mix. Rigids were weaker, particularly in North American PET in Q4.

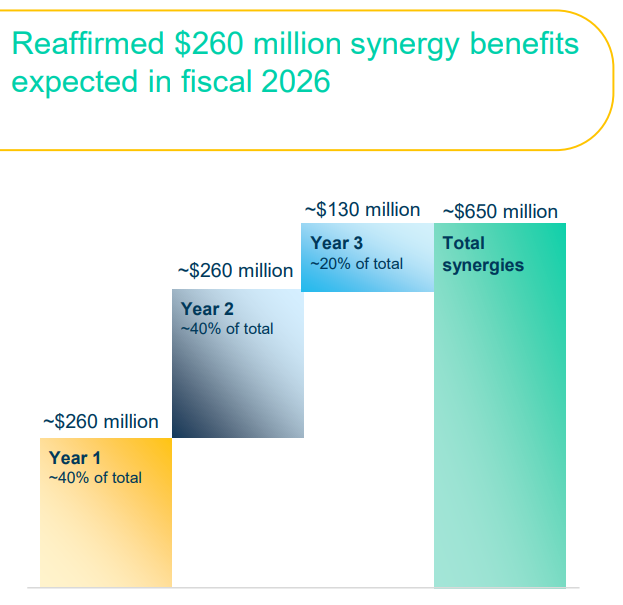

- Berry Merger: Amcor completed its merger with Berry at the start of April, contributing two months of earnings to Amcor’s results. Over the next three years, the merger is expected to create $650 million in synergies and widen Amcor’s packaging options to include containers and closures, which are highly complementary to Amcor’s flexibles range (See Below). In the last few months, AMC announced that it has cut headcount by over 200 and is closing five of the acquired sites.

- Strong Balance Sheet: AMC’s balance sheet remains strong, with 3.5x leverage, well within the expectations of what this type of business can handle. Management is guiding that leverage will be below 3x over the coming year, as some divestments are expected to flow through the business. In particular, AMC are looking to divest North American beverages and excess assets acquired from Berry.

- Dividends Up: AMC announced a dividend of US$0.51 per share, representing a 2% increase from last year.

- Guidance: AMC management provided earnings guidance for next year of 80-83 cents per share, representing 12-17% earnings growth. Management believe the synergies coming from the Berry merger will deliver $260 million in cost savings next year.

- Why is the stock down? The last quarter’s volumes came in weaker compared to previous years, largely due to a weaker North American Beverage season, which saw revenue and earnings lower than market expectations. Amcor is undergoing a strategic review of its business lines to find accretive divestments and focus on its core packaging offering. Atlas have a meeting with CEO Peter Konieczny late next week to discuss the result and AMC’s path to earnings per share growth of 12-17% in FY26.

Portfolio Strategy: Amcor is the largest global packaging company with operations in 43 countries. While packaging is not the most exciting of industries, Amcor exposes its portfolio to global growth in consumer and medical goods, as well as manufacturer demands for increasingly sophisticated packaging. 95% of AMC’s customer base is in consumer staples, including packaging for meat, cheese, sauces, and condiments, as well as beverages, coffee, pet food, healthcare, and personal care products, all of which have stable defensive characteristics. AMC trades on a PE of 10x with a full-year dividend yield of 6%. Nothing in this result changes our investment thesis that Berry was a good acquisition for AMC, setting the company up for strong near-term earnings and dividend growth.

AMC finished down -9.6% to $13.60 – with the market focusing on weaker Q4 volumes rather than guidance in a result that was tough to analyse. I have been following this company for over 20 years, including several years covering AMC on the sell side, and this one was particularly tough to untangle.