Last night, Ampol (ALD), Australia’s largest energy distributor and retailer, announced that it is offering to buy EG Australia. The HNW Portfolio has a 4% weight to ALD.

Key Points:

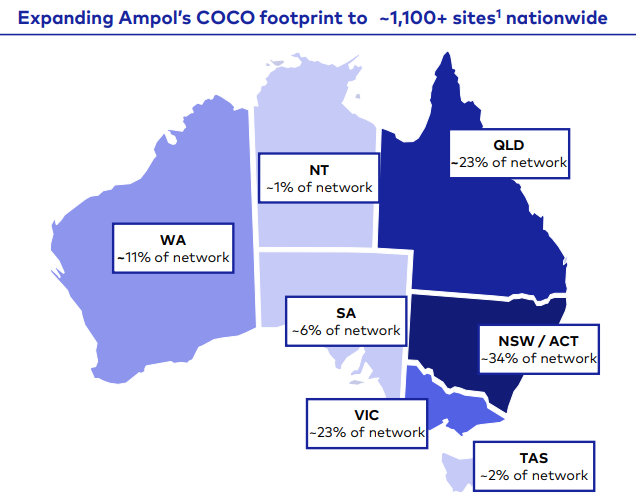

- The Deal: ALD is looking to acquire EG Australia for $1.05 billion, comprising $800 million in cash and $250 million in scrip. EG Australia has 500 sites, with the majority located in the eastern states of Australia (See Below). Approximately 125 sites are slated for conversion into U-GO sites, Ampol’s unmanned service offering.

- The Acquisition Makes Sense: The acquisition will give ALD higher penetration in its East Coast offering, as well as create a new offering of premium Foodery sites and higher-margin, smaller U-GO sites. The acquisition will also push Ampol’s earnings further away from the volatility of fuel refining to the more consistent and stable retailing business.

- Balance Sheet: Following the acquisition, Ampol’s leverage will be 3.0x above its target leverage range of 2.0-2.5x, but will quickly fall back into range following a full year of ownership of the new sites. Atlas looks at this as the preferred method for the transaction over an aggressive capital raise.

- Will the ACCC coming knocking? Unlikely, as part of the proposed acquisition Ampol has already committed to divest approximately 20 EG sites which are located near already owned Ampol sites, which will likely appease the regulator.

- Why is the stock up? The stock is up due to the acquisition, which strategically aligns with Ampol’s ambition to grow its profits away from the volatile earnings of fuel refining, as well as investing in and transforming more sites into higher-margin unmanned sites. ALD appears to have acquired these assets at a bargain price of 5.8x EV/EBITDA from a motivated seller who needs to raise cash due to issues elsewhere in the sprawling EG empire.

Interestingly, in 2020, EG offered to buy Ampol’s (formerly Caltex) convenience retail business for $3.9 billion, or $35 per share, after paying $1.7 billion for Woolworths’ fuel business in 2019. It is a great outcome for ALD to acquire that business for a significantly more attractive $1.1 billion today.

Portfolio Strategy: ALD is the core energy exposure in the Portfolio but with greater exposure to fuel and food retailing rather than the vagaries of the oil price. Over the past five years, ALD has changed from a capital-intensive business with volatile earnings dependent on global refining margins to one increasingly based on fuel and convenience retailing and bringing franchised service stations in-house. ALD trades on an undemanding = 15x forward earnings with a 5% fully franked dividend yield.

ALD finished up +7.7% to $29.15, following the announcement of the acquisition and ahead of its results release on Monday