Macquarie Group (MQG): This morning, the global investment bank reported its first results for 2025, which were solid despite half having much fewer investment banking deals and reduced energy price volatility in the marketplace. HNW Growth and Income Portfolios have 7% and 6% weights to Macquarie Group.

Key Points:

- Profits Up: First-half profits were up 14% to $1.6 billion, driven primarily by Macquarie Asset Management and Banking and Financial Services, which benefited from strong public market return and growth In home loans.

- Macquarie Bank: Profit from the bank increased by 2%, driven by a 9% increase in their home loan portfolio to 5.6% of Australian mortgages. Macquarie management that they are seeing more competition for mortgages but that their growth in both deposits and loan offset the lower margin.

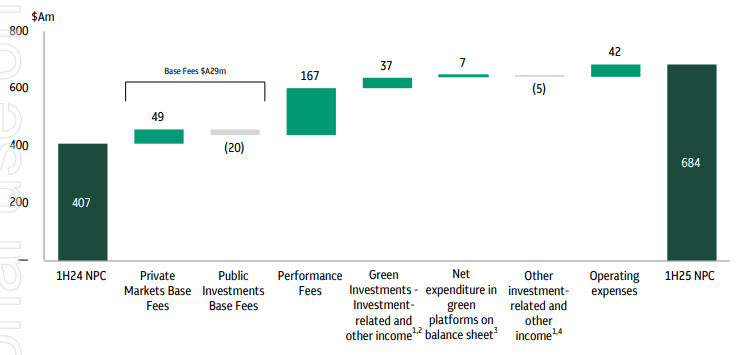

- Asset Management: Profits from Macquarie Asset Management increased by 68% following strong performance from their fund managers and delivering an increase of $157 million in performance fees for the half. Macquarie also benefitted from increased management fees from moving some of their green asset off their balance sheet and into managed funds. (See Below)

- Dividends Up: Macquarie management announced a dividend of $2.60 (35% franked), representing a +2% increase in the first half of 2024.

- On-market Buyback: Macquarie has completed $1 billion of on-market share buybacks, with $1 billion to be still completed of the $2 billion announced in November 2023.

- Guidance: Macquarie management did not provide any full year guidance for any of the businesses but did state that they remain with a cautious stance for global markets and well positioned to respond to a change in the current environment.

- Why is the stock down? The stock is off today due to lower earnings from the commodities business, which as caused to lower volatility in global energy prices due to a larger global supply of energy with little to no disruptions during the half. MQG is the largest energy trader in the USA and historically has derived high profits from large swings in the oil and gas prices and prices were relatively stable over the past six months

MQG finished down 3.6% to $223.20, although Macquarie has been a solid citizen in the Portfolio up 24% in 2024 (vs 10% ASX 200).

CEP Strategy: Atlas’ preferred bank exposure is Macquarie Bank, which offers exposure to a global investment bank with a heavy weighting towards stable funds management earnings and will benefit from a falling AUD. Unlike the major trading banks that operate in a competitive oligopoly where any moves to grow market share are swiftly matched by the other banks, Macquarie’s growth is not constrained by Australian GDP growth, with 65% of revenue coming from international markets.

MQG offers investors both the “cake” of stable annuity-style profits from asset management to go with the “icing”, that is, the more volatile earnings that are derived from investment banking and trading in commodities and financial markets. This was a steady result from the “vampire kangaroo “which trades on an undemanding PE of 18x with a 4% yield.