Wesfarmers (WES): This morning, the last conglomerate on the ASX, presented its half-year 2026 results, demonstrating that WES’s businesses are performing well, taking market share. Given current valuations, it was always going to be tough for WES’ share price to be up today. The HNW Portfolio has a 3% weight to WES.

Key Points:

- Record Profits: Earnings increased by 9%, to $1.6 billion, driven by a 6% increase from Kmart group (Kmart & Target) earnings, which benefited from the ongoing digitalisation of operations. Bunnings profits were rock solid, up 5%. WesCEF (Chemical, Energy and Fertiliser) and Health posted strong double-digit earnings growth, offsetting a fall in Officeworks earnings.

- Anko Going Global: Following a review of the global expansion of Anko, Wesfarmers has decided to roll out stores globally for the Anko offering rather than being a wholesale provider. Anko currently operates 5 stores in the Philippines, which they plan to use as a launch pad for further expansion into Southeast Asia.

- Balance Sheet: WES has a very strong balance sheet with a net debt position of $4.9 billion. This is a business that can handle that level of debt, with Debt/EBITDA at 1.7x below the target range and debt costs being a low 3.6%.

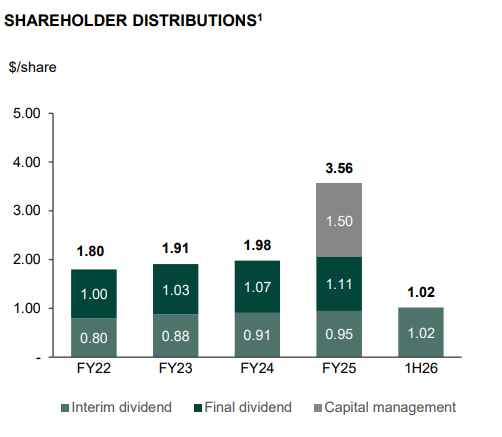

- Dividends Up: Wesfarmers announced a half-year fully franked dividend of $1.02, up 7%, continuing a progressive dividend policy (See Below). WES also announced that they will be neutralising their Dividend Reinvestment Plan and purchasing the shares on the market.

- Guidance: Wesfarmers did not provide any specific guidance for the rest of the year but did disclose that Bunnings is continuing its strong sales growth in the first weeks of the second half, with Kmart growing sales more quickly over the same time period.

- Why is the Stock Down? Wesfarmers has been priced for perfection heading into the result, with a lot of focus being on the ability for Wesfarmers to grow profits when higher mortgage rates crimp consumer spending.

Portfolio Strategy: WES give the portfolio exposure to a stable, diversified stream of earnings exposed to the Australian economy primarily through hardware (Bunnings), office supplies (Officeworks), discount department stores (Target and Kmart), pharmacy (Priceline), chemicals and, in the near future, lithium. WES is a very well-run company, with CEO Rob Scott consistently making good moves for shareholders since taking over in 2018. In the Portfolio, we only own the retailers that dominate their markets (Wesfarmers and JB Hi-Fi) and are the lowest-cost operators. This result from WES shows that value-conscious consumers are still happy to open their wallets. Late last year, we reduced the WES position to higher levels.

WES finished down -5.6% to $84.24, on what was largely a positive result