QBE Insurance (QBE): The global insurer released its full-year 2025 profit results, confirming the continuation of positive trends in the insurance industry with increasing premiums, lower claims inflation and benefits from the company cleaning up the business. Overall, an excellent result from QBE. The HNW Core and Income Portfolios have a 4.5% weight to QBE.

Key Points:

- Record Profits: QBE’s net profit was up +23% to US$2,132 million, driven by a combination of a 7% increase in premiums, prudent underwriting, solid investment returns and lower than expected catastrophe claims. Over the year, QBE benefited from a benign Atlantic hurricane season and side-stepping the 2025 California wildfires after exiting insuring assets in the state after price caps were introduced a few years back. This delivered QBE’s best-ever result, with a return on equity of 20%. QBE’s previous high-water mark was 2006, which was boosted by some questionable global acquisitions that took over 10 painful years to unwind.

- Investment Float: The net return on QBE’s US$36 billion investment float in the half was US$1,633 million, representing a 4.9% annualised return. Here, QBE is seeing a tailwind from higher interest rates.

- Strong Balance Sheet: The balance sheet remains in good shape, with its regulatory capital above the top end of the range at 1.87x (1.6-1.8x), which will be reduced via a share buy-back and higher dividend. Gearing low at 24%.

- Dividend Up: Up +25% to $A1.09 per share, additionally, the company will buy back $450M of shares on market over 2026.

- Outlook: Management has guided to 5-10% premium growth for 2026, lower investment yields and 15% ROE. Overall, management was more confident than usual on the call, reflecting the simplification of QBE’s business.

- Why is the stock up? Result ahead of market expectations, and QBE, along with other insurance stocks, have been weak based on the theme that AI is a threat to the business. Given the heavily regulated nature of the business and the vast capital requirements, it is hard to see how AI can take over insurance underwriting. Indeed, QBE discussed how AI is already unlocking value for the insurer by improving efficiency in the claims process, fraud detection and pricing.

QBE finished up 7% to $21.48

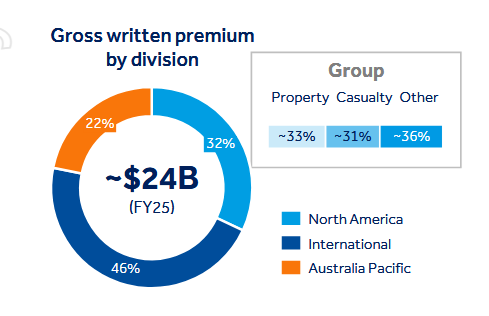

Portfolio Strategy: QBE has a diverse class of insurance business lines across Australia, Asia, Europe and America and gives the portfolio exposure to both a falling AUD, rising interest rates and a hardening of insurance pricing globally. This result shows the benefits of the simplification drive over the past five years, which has seen QBE jettison exotic businesses such as Argentinian workers comp, Colombian third-party motor, and Ecuadorian crop insurance acquired during QBE’s growth at all costs phase 15 years ago. QBE is managing inflation well by pushing through premium increases and is benefiting from rising rates.

QBE still looks undervalued, trading on a forward PE of 10x with a 5.5% yield