Sonic Healthcare (SHL). This morning, global pathology company SHL reported their first half 2026 which were in line with our expectations but ahead of the more pessimistic sell-side analysts. The HNW Portfolio has a 3% weight to Sonic.

Key Points:

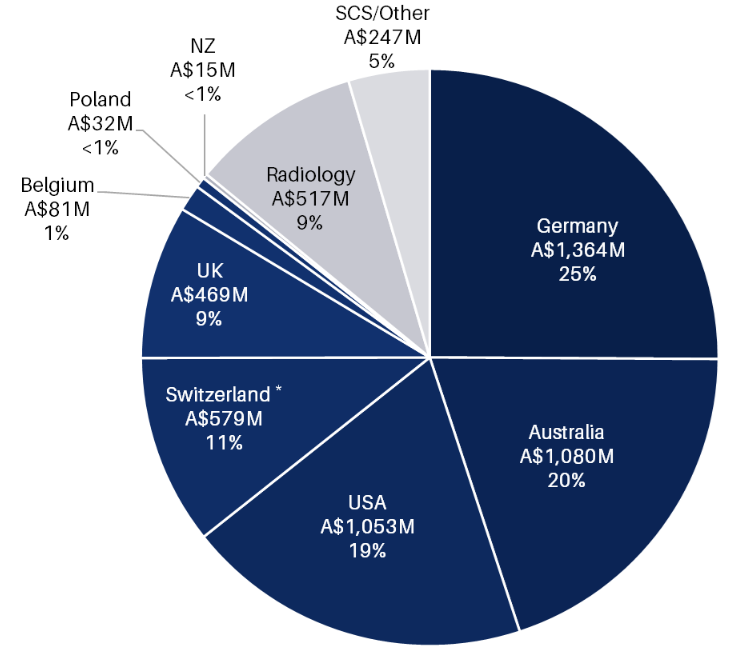

- Record Profits: Profits increased by +11% to $262 million. Generally strong across all segments of the Sonic global business. The highlights for us were Germany, contract wins in the UK and the USA, with a contract loss in Alabama being offset by a win in New York. Australia and Switzerland grew steadily, but interestingly, Australia has now been overtaken by Germany as the largest segment.

- Cashflow Strong: operating cash generated up +10% to $682 million

- Dividend: A modest increase of +2.3% in the interim dividend to $0.45 per share, in line with SHL’s progressive dividend policy supported by strong cash generation. The sale and lease-back of the SHL Brisbane hub laboratory is expected to generate around $475M, which will be used to fund an on-market share buy-back.

- Continued Balance Sheet Strength: Gearing at 29% with an interest cover ratio (annual profit divided by interest cost) of 10 times, there are no anxious bankers. Gearing a little higher due to acquisitions in New York and northern Germany.

- Why is the stock up? In August, the market was very sceptical that SHL would achieve their profit growth targets in 2026, despite having what we saw as a clear path to do so. This result showed both organic growth and acquisitions contributing to profits.

- Outlook: Sonic management confirmed guidance for profit growth of +13% for 2026, based on organic growth and acquisitions in Germany and the UK.

Portfolio Strategy: Sonic exposes us to the rising demand for medical testing, exacerbated by new medical technologies, an aging population, and doctors’ desire to cover themselves against malpractice claims by increasing the number of tests ordered. SHL is the largest global patient testing company, ranking #1 in pathology in Australia, Germany, and Switzerland, #2 in the UK, and #3 in the USA. Unlike drug companies or device companies, such as Cochlear, SHL has an industrial process for blood and tissue sample testing that benefits from economies of scale, rather than the hundreds of millions of dollars invested in R&D to develop the next wonder drug or device.

At current prices, SHL looks cheap, trading on a PE of 16x with a yield of 5.3%.

SHL finished up +10% to $23.33.