This morning, Whitehaven Coal (WHC) provided its half-year results for 2026, which were slightly below market expectations, given that it provided a trading update in late January. The HNW Portfolio currently holds a 3.8% weight in WHC.

Key Points:

- Profits Down: Whitehaven recorded a 31% fall in profits to $69 million, driven primarily by a fall in the price of metallurgical coal (-14%) and thermal costs (-20%). Whilst coal prices were subdued, WHC demonstrated operational excellence across their portfolio, and is well on its way to stripping out a further $60-80 million out of the business on top of the $100 million from last year.

- Strong Balance Sheet: WHC currently has A$710 million in net debt, representing a gearing ratio of 11%, and a leverage ratio of 0.8x. This provides WHC plenty of flexibility in the balance sheet to continue to focus on operational excellence.

- Dividend Down: WHC announced a half-year fully franked dividend of 4 cents per share. This is expected to pick up substantially in the second half of the year, buoyed by strong increases in coal prices in the last 6 weeks.

- On-Market Share Buyback: WHC management announced that their $75 million share buyback from the first half was complete and announced they will start another $32 million buyback for the second half of FY26.

- Guidance: WHC management reaffirmed guidance that they expect to produce 40 million tonnes of coal next year with a group cost of A$135/t.

- Why is the Stock Down? The stock is down following a small downgrade to the longer-term cost for the Queensland mines due to inflation. While this is disappointing, WHC management has four cost levers they can pull to rain in these costs over the next few years. At current commodity prices in 2026, WHC is very profitable.

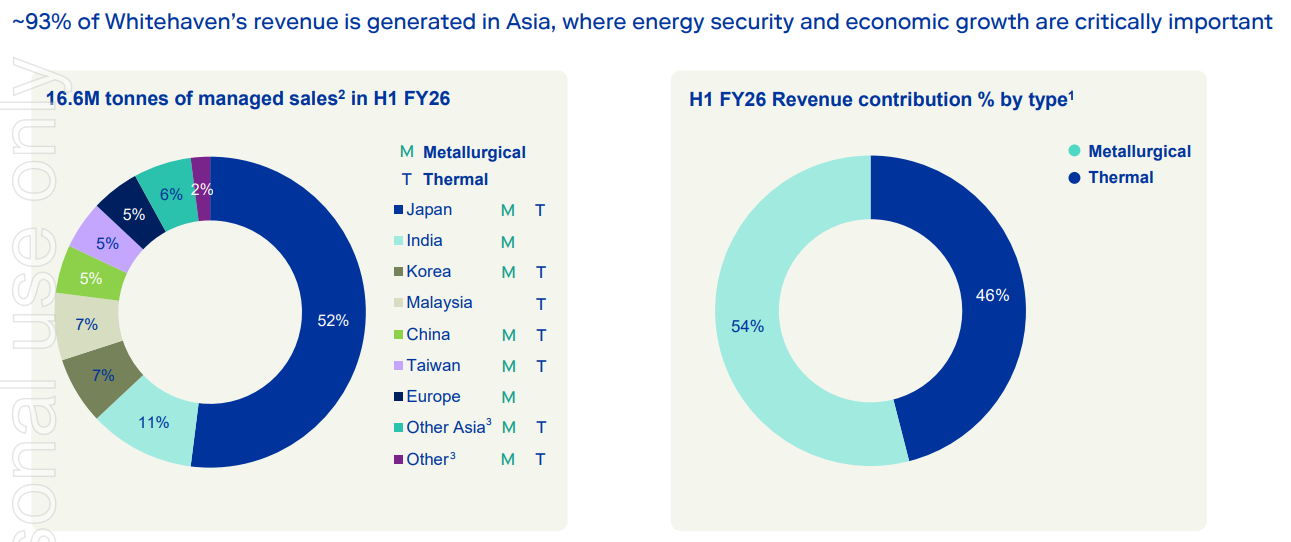

Portfolio Strategy: Whitehaven has undergone a transformational acquisition, which has seen the business move from a pure thermal coal miner to a combined metallurgical (steel) and thermal coal business. This acquisition from BHP grants Whitehaven access to new mining assets with 50+ years of mine life at a very low price of 1.9 times earnings and will see a significant increase in company profits regardless of any downward moves in the coal market. Whitehaven thermal coal mines produce one of the highest quality coal exported mainly to Japan, with low ash content, meaning that Whitehaven coal collects a premium to international pricing and that these mines will be the last mines to close down. WHC trades on 12x earnings and a 3.5% dividend yield based on a 50% payout ratio.

WHC finished down -4.8% to $8.03, but has been a solid citizen of the portfolio, return +58% over the last 12 months.