This morning, Woodside (WDS) reported its full-year 2025 results, which were around +5% ahead of expectations. Overall, a solid result from Australia’s largest energy company. The HNW Core Portfolio holds a 4.5% weight to WDS.

Key Points:

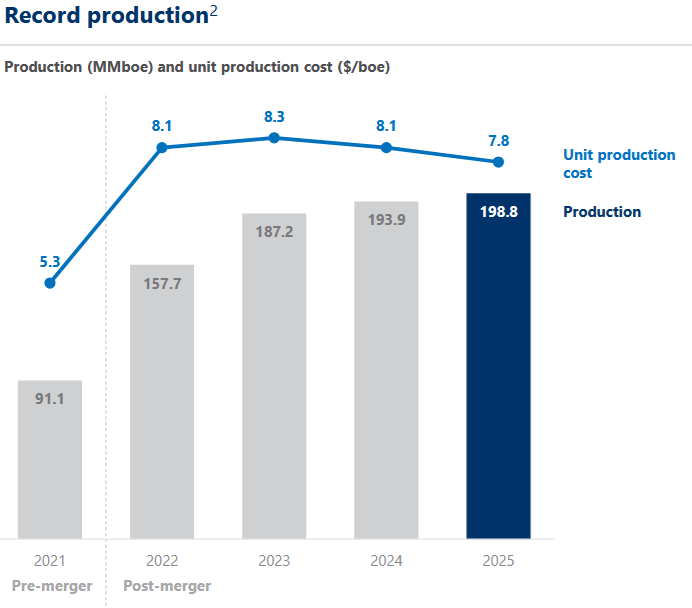

- Profit: Net profits of US$2,649 million, am 8% decrease over last year reflecting a fall in the oil price. Pleasingly, 2025 saw production reached a record 199 million barrels of oil, and unit costs fell 4% to US$7.80 per barrel – this was 2 million barrels ahead of guidance. Falling unit costs were due to a 99% LNG plant asset reliability and the full impact of the new Sagomar field in Senegal, which is proving to be a very solid development for WDS.

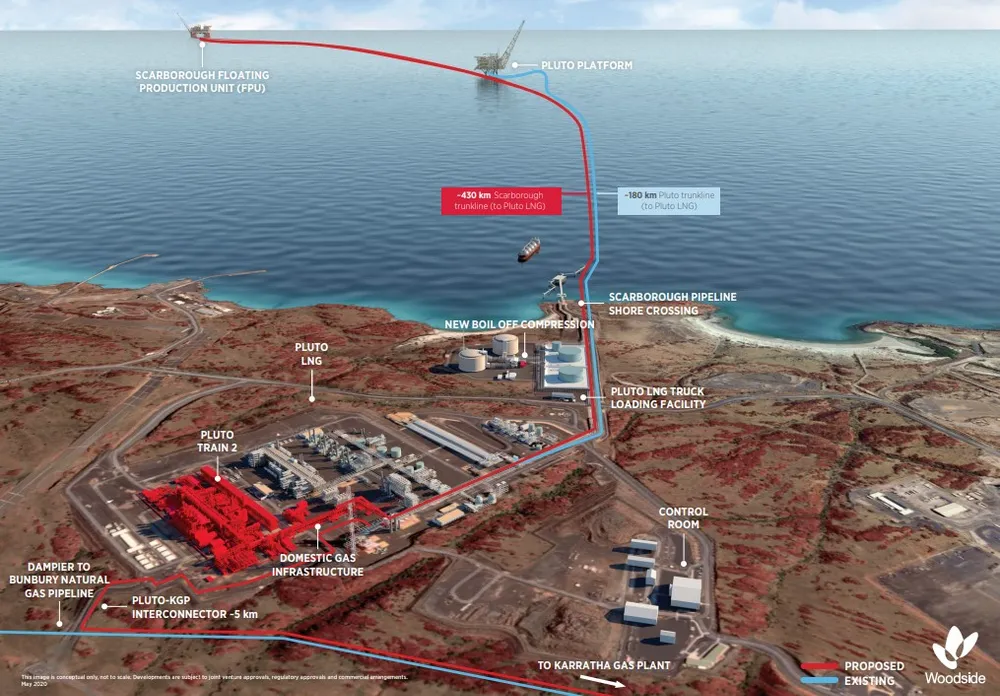

- More Growth to Come: WDS have been very busy in 2025 with new assets under construction progressing well. Scarborough LNG is 94% complete, with the first LNG targeted for early 2026, and will be processed at WDS’ existing Pluto infrastructure in Western Australia rather than building new LNG processing plants. Trion in the Gulf of Mexico is 50% complete and is targeting first oil in 2028 and Louisiana LNG is targeting first LNG in 2029, with sell downs to JV Partners StonePeak & Williams paying WDS US$2.1 billion and contributing to US$7.6 billion to the construction cost.

- Balance Sheet: Woodside maintains a strong balance sheet, with a 18% gearing ratio. This is very impressive and reflects the company reducing project risk and capex spend by selling down equity stakes in projects to offtake partners.

- Dividends: The final dividend of US$0.59 was ahead of expectations and up +11% on 2H last year.

- Guidance: WDS guided that they expect to produce 170-183 million barrels of oil in 2026, with the reduction on 2025 expected and due to maintenance on Pluto LNG train, as well as connecting the new Scarborough LNG to be processes at the existing Pluto on-shore infrastructure (see table on the right), thus improving the economics of the project. Further sell-down of a stake in the US LNG export terminal is likely and

Portfolio Strategy: WDS is the Portfolio’s sole energy producer and is the most conservative and well-managed Australian oil company with no exposure to the problematic and politically charged East Coast gas market. WDS has the lowest production cost and gearing, which is a crucial position for an energy company, given that market conditions can change abruptly. WDS provides insurance in the Portfolio against a major US strike on Iran.

WDS trades on a very undemanding PE of 13x with a 5.9% fully franked yield.

Woodside finished up +2.4% to $27.75