Region Group (RGN): This morning, Australia’s largest convenience mall landlord, RGN, released its half-year results for 2026, and the results were largely in line with expectations. Though given the nature of RGN’s assets, full occupancy and long leases, there is minimal scope for negative surprises. The HNW Income Portfolio has a 2.5% weight to RGN.

Key Points:

- Profits Up: Regions Funds From Operations (FFO) was up 4% on last year to $91 million, with increases in long-leased property rents being slightly offset by interest and corporate expenses.

- Distributions Up: Distributions were up +3% on last year to 6.9 cents per share

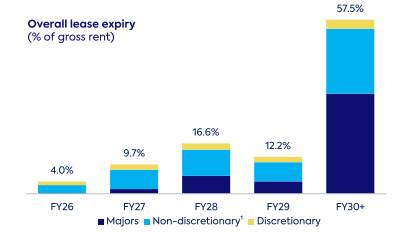

- Operational Performance: RGN continues to manage its portfolio well, with occupancy at 98% and a strong average lease term of 4.8 years, with minimal near term expiries. Tenant sales in the centres remained strong, with sales increasing by 3.1%, led by Medical & Beauty (+6.2%), Discount Department Stores (+3.7%) and Food & Liquor (+3.4%). Currently, 52 or 53% of supermarket anchors are paying turnover rent in addition to base rent, consistent with last year.

- Balance Sheet: Interest rate hikes present no near term problems for RGN as gearing is currently at 32%, at the low end of the target range of 30-40%. 100% of company debt is either hedged or at a fixed rate. RGN currently has an average debt cost of 4.6% and an average debt maturity of 4.3 years, with no debt expiring until 2028.

- Valuation: NTA increased by 9 cents per share to $2.56, driven by increased valuation of investment properties in combination with an on-market share buyback reducing outstanding shares.

- Outlook: RGN management upgraded guidance for 2026 to Funds from Operations of 26 cents per share, representing an increase of 3%, bolstered by the resilient nature of non-discretionary spending and rent growth. This equates to a yield just over 6%.

Portfolio Strategy: RGN offers the portfolio exposure to non-discretionary retailing via a diversified portfolio of neighbourhood shopping centres typically anchored by a Woolworths or Coles supermarket with an accompanying Dan Murphy’s or BWS. Unlike better-known retail landlords such as Scentre or Stockland, RGN’s tenants are not particularly exposed to the impact of online sales or the Coronavirus impacting tourism, with consumer staples and alcohol, as well as medical and personal services such as haircuts, are not easily delivered online and bought almost entirely by local Australian residents. Long leases to quality tenants such as Woolworths, Coles and Aldi give a high degree of confidence that RGN can maintain and grow its distributions over time.

RGN finished up +0.5% to $2.33

Greystanes Shopping Centre NSW