Commonwealth Bank (CBA) reported its full-year results for 2025, which showed that the underlying business was operating solidly as Australia’s largest company. Due to the breadth of its lending activities, which touch every sector, CBA is closely watched for a read on the broader Australian economy’s health. The HNW Portfolios have an 8.8% weight to CBA (index weight 11.1%).

Key Points:

- Record Profits: CBA reported profits increased by 4% to $10.3 billion, following gains in market share across both retail and business banking. Looking more closely at the result, it appeared that CBA might have been trying to minimise their headline result by substantially increasing their discretionary technology spend. CBA announced an increase in technology and AI spending, which rose to 18% of $1.2 billion. For context, NAB spent less than half ($520 million) on technology and systems last year.

- Net Interest Margin Up! Over the year, CBA’s net interest margin increased by 0.09% to 2.08%, with deposit competition offset by a higher contribution from higher margin products and equity hedges. During the call, management highlighted that they expect their margins to be negatively affected by the interest rate cuts, but still remain well above those of other banks (NAB: 1.70%). While this move may seem minor, CBA generated an additional $1.2 billion in interest income from its $1.15 trillion loan book as a result of this small adjustment. Small gains matter.

- Bad Debt Remains Low: Declining to 0.07% of Gross Loans, Well Below the Long-Running Average of 0.3%. While unemployment remains low, Atlas expects banks’ loan losses will remain low, particularly when much of the more “exciting” high-yield lending to developers is not on bank balance sheets but rather with Private Credit Funds.

- Capital High: Tier 1 capital high at 12.3%, which will be built by a further $1 billion after the sale of its remaining stake in the Bank of Hangzhou. Currently, CBA has $700 million left over from its $1 billion on-market buyback, which was last executed on November 15th of last year. Management is understandably reticent to buy back shares at current prices, so they will either keep their powder dry for a pullback or return capital via a special dividend in February.

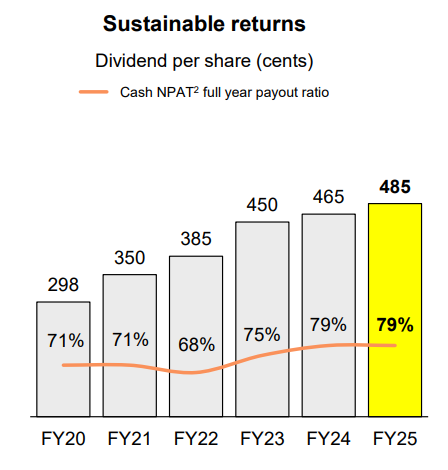

- Dividend up: CBA announced an interim fully franked dividend of $4.85 (See below), representing a 4% increase on last year. CBA also announced that it would fully neutralise its Dividend Reinvestment Plan (DRP), meaning that current investors are not being diluted, as CBA will buy roughly $450 million worth of CBA shares before distributing them to investors.

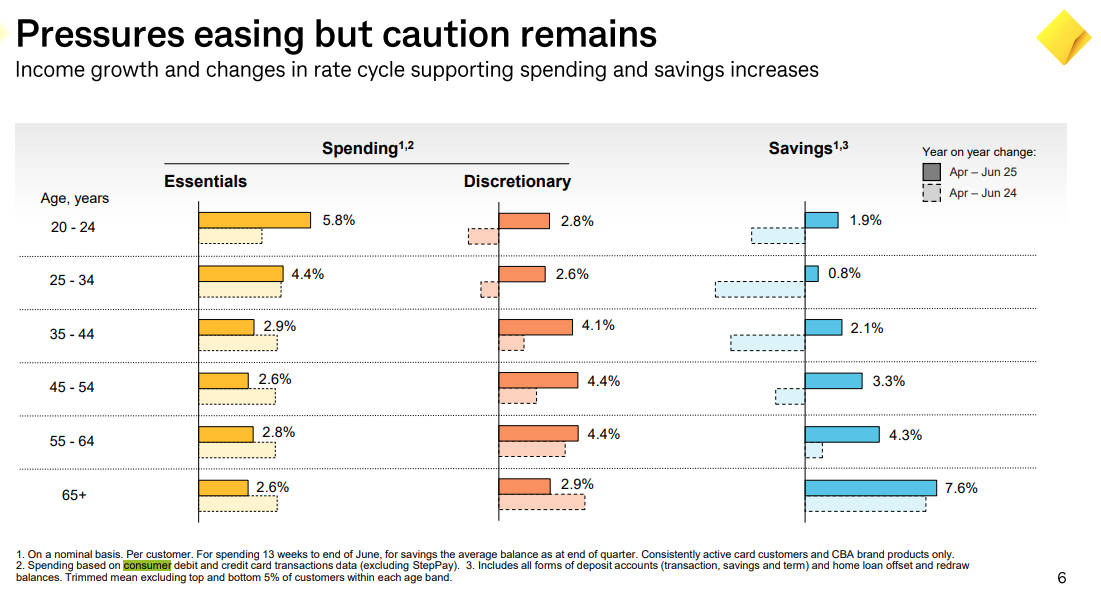

- Outlook: No direct profit guidance was provided, but management discussed improving conditions across their client base (1 in every 3 Australians) – see the chart on the right, which shows income growth and falling rates leading to increases in savings and spending for all cohorts except those aged 65+.

Portfolio Strategy: Following this result, Atlas maintains its view that CBA is the best bank in Australia; however, it is currently trading at a very expensive multiple, which has led Atlas to position CBA as a portfolio underweight. What to do with the banks in 2025 has been a key question for investors, as global investors started buying instead of shorting the Australian banks. Atlas have been slower than most fund managers to reduce our banks exposure due to the combination of buy-backs, lower for longer bad debts and

This result demonstrated the resilience of the CBA’s key profit centre, retail banking services, as high employment and a cleaner corporate loan book compared to 1991 or 2007 will result in lower bad debts (and higher profits) than the market expects. CBA is a well-capitalised Australian bank with a Tier 1 ratio of 12% after the dividend, and most of a $1 billion buyback ($700 million) remains to be completed. In the event of further weakness, we may consider repurchasing some of the CBA we sold in June.

CBA finished down -5% to $169.12, but Atlas continues to have an underweight position towards CBA