This morning, Suncorp (SUN), the now pure-play East-coast insurer, delivered strong full-year 2025 results and revealed how it will reward shareholders from the sale of its bank and continued strong cash flows. Overall, a very solid result. The HNW Portfolio has a 3% weight to SUN.

Key Points:

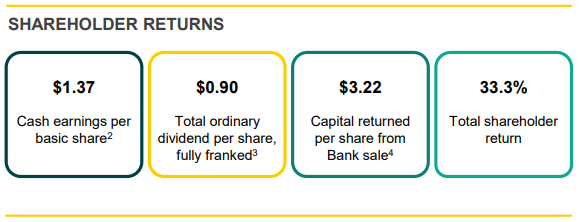

- Record Profits: Suncorp profits were up +44% to $1.4 billion, driven by strong insurance underwriting in both their Australian Consumer and New Zealand insurance offerings. SUN businesses have enjoyed a perfect storm of 1) low natural hazards, 2) rising premiums, 3) a slowdown in claims inflation, particularly in New Zealand, following the floods and 4) higher investment yields.

- Natural Hazards Benign: In 2025, SUN reported natural hazards of $1.35 billion, which was below the expected $1.6 billion. Interestingly, SUN have increased its allowance next year to $1.8 billion, reflecting the growth of the business and the company’s conservative approach. Over the past 10 years, SUN has overestimated cat claims in 7 out of the 10 years, resulting in cumulative favourable flows back to shareholders of $1.5 billion.

- Rock-solid Capital Position: SUN continues to maintain a very strong balance sheet with a capital ratio of 1.80x, well in excess of the target range of 1.025x-1.325x. This equates to $900 million of excess capital.

- On-Market Share Buyback: Following its strong capital position, SUN announced an additional $400 million on-market share buyback to be completed over the next year. Management also commented on the call that it is highly likely that another share buyback of a similar size will be announced for 2026. This buyback is also in excess of the capital return from the bank sale of $3.22 a share earlier this year. (See Below)

- Dividend Up: SUN announced a fully franked dividend of $0.90, representing a payout ratio of 71% of cash earnings and a +15% increase on last year’s dividend. This is the best dividend result for Suncorp since the GFC in 2008!

- Outlook: SUN management provided solid guidance, with the number of premiums expected to increase by mid-single digits as claims inflation continues to moderate across the business. Ongoing buybacks and simplifying the business into a pure-play general insurer have seen SUN re-rated by the market.

CEP Strategy: SUN is now a pure domestic insurer providing portfolio exposure to rising insurance premiums across Eastern Australia as well as higher interest rates. We have preferred SUN over IAG as our domestic insurance exposure, as it is significantly cheaper, and we like the potential for further capital returns after the bank capital return and the strong cash flows in the coming years. SUN trades on 17x forward earnings with a 4.5% yield.

SUN finished up 3.6% to $20.77.