A mixed month in relative terms, dominated by a very volatile reporting season.

In a quick note vis-à-vis the situation in Iran, in both Portfolios we have significant exposures to energy – 17% in the Income Portfolio and 14% in the Core via Woodside, WhiteHaven & Ampol – all three are up +8% in March on spiking energy prices.

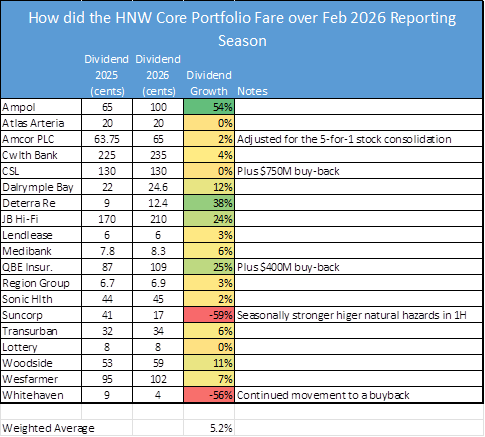

The HNW Core Portfolio gained by +2.65%, trailing the benchmark return of +4.1%, a disappointing outcome as we were ahead of the index up until the final week of the month. Not owning BHP was the main contributor to underperformance, along with CSL, which will be discussed at the IC meeting yesterday. The Big Australian hit all-time highs in February and was up +16%, an amazing move as current earnings exclude the S32 assets that were spun off, along with the $13.8 billion of petroleum assets that currently sit with Woodside, and iron ore has fallen 10%. BHP trades at a PE of 21x with a 3% yield – a peak valuation.

Over the month, positions in Woodside (+12%), QBE (+10%), Amcor (+10%), Westpac (+10%) and ANZ (+9%) added value. On the negative side of the ledger, CSL (-19%), Suncorp (-13%) and Whitehaven (-11%) hurt performance along with the underweight to CBA (+18.5%) and BHP.

More pleasing was the income situation for the HNW Core Portfolio, which saw the weighted average dividend declared increase by 5.2% ahead of inflation. We view the change in dividends as a key earnings quality measure, giving us more meaningful insight into the outlook for a company than headline profits or statements from the CEO.

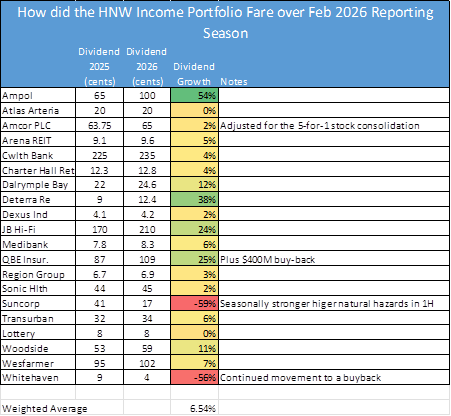

In February, the HNW Income Portfolio had a solid month, +3.57% ahead of its blended benchmark return of +2.23%. Over the month, positions in Woodside (+12%), QBE (+10%), Amcor (+10%) and added value. On the negative side of the ledger, performance was hurt by WhiteHaven (-11%), Dyno Nobel (-5%) and Arena REIT (-4%).

In February, the HNW Income Portfolio saw the weighted average dividend declared increase by 6.5% for the past six months, was a pleasing outcome.