This morning, Suncorp (SUN), the now pure-play East Coast insurer, delivered solid half-year 2026 results that were impacted by higher hailstorms on what was a good underlying result. The HNW portfolios has a 2% weight to SUN.

Key Points:

- Profits Down: Suncorp’s half-year profits were down to $270 million, driven by a one-off increase in natural hazards. The underlying business has been operating well, with the business growing profits by 6% outside of natural hazards, driven by a 7% increase in home insurance pricing and a 6% increase in motor insurance.

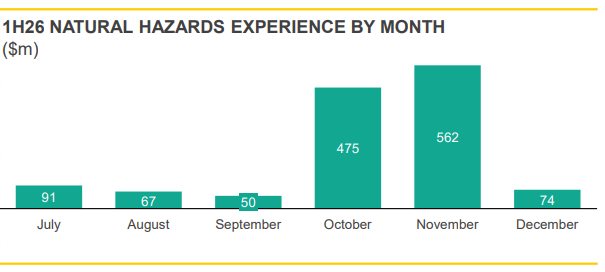

- Natural Hazards: Over the last six months, the east coast of Australia and New Zealand has experienced 9 natural hazard events totalling $1.3 billion in damages and costs. The heightened costs were dominated by tropical storms in South-East Queensland over October and November (See below) that saw hailstones up to 14cm in diameter. While annoying for shareholders and stressful for policyholders, without storms and property damage, there would be no need for insurance.

- Strong Capital Position: SUN continues to have a very strong balance sheet with a capital ratio of 1.81x, or $700 million in excess of the target range of 1.025x-1.325x.

- Dividend: SUN announced a fully franked dividend of $0.17, representing a payout ratio of 68% of cash earnings, a prudent move given the heightened volatility of natural hazards. In conjunction with this dividend, the $400 million on-market share buyback will continue post results.

- Outlook: SUN management reiterated solid guidance, with the number of premiums expected to increase by mid-single digits as claims inflation continues to moderate across the business. SUN management also stated that during both January and the start of February, natural hazards were within the monthly allowance.

CEP Strategy: SUN is now a pure domestic insurer providing portfolio exposure to rising insurance premiums across Eastern Australia as well as higher interest rates. Whilst it is disappointing to see a high level of natural hazards impacting profits, these weather events will cause more people to get their houses and cars insured at a high premium price point. We have preferred SUN over IAG as our domestic insurance exposure as it is much cheaper, is supported by strong cashflows in the coming years and has the potential to benefit greatly from AI innovation. SUN trades on 13x forward earnings with a 5.5% yield.

SUN finished down -4% to $15.28