Amcor (AMC). This morning, the world’s largest consumer packaging company & JA’s least favourite stock announced its results for the first quarter of 2026, marking the first full quarter of operations following the Berry Merger. The HNW Core Portfolio has a 4.2% weight to AMC.Key Points:

- Profits Up: First-quarter earnings per share increased by +18% to $687 million, with higher profit margins and synergy benefits from Berry offsetting a 2% decline in volume. Amcor management expects the business to return to growth over the coming year, following the Berry merger, as it can now manufacture more products at higher margins. (See Below)

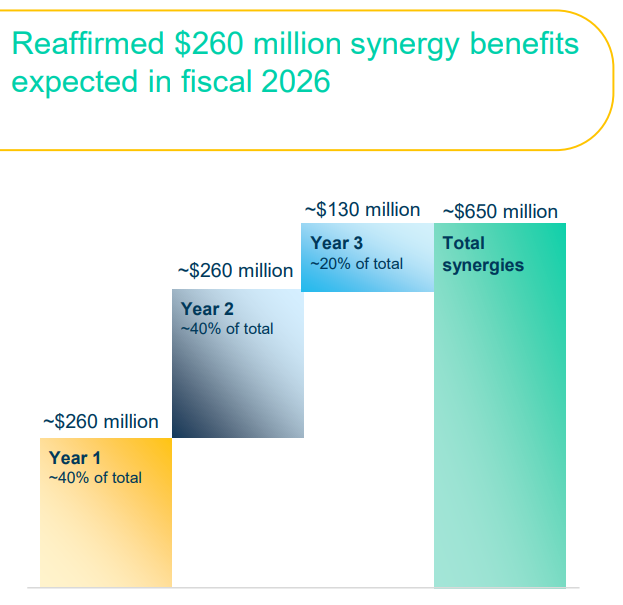

Berry Merger: Amcor completed its merger with Berry earlier this year, with this result marking the first full quarter of the combined business. The merger resulted in sales increasing by nearly 70% and earnings rising by 85%, while also improving the profit margin over the quarter. Amcor has begun realising some of the synergies from the merger ($33 million in the first quarter), with $650 million in synergies to be realised over three years. - Dividends Up: AMC announced a quarterly dividend of A$0.20 per share, representing 2% growth on last year.

- Guidance Reiterated: AMC management reiterated their earnings guidance for next year of 80-83 cents per share, representing 12-17% earnings growth. Management is confident that the synergies resulting from the Berry merger will deliver $260 million in cost savings next year.

- Why is the Stock Up: The stock is up following management’s clear expectations of achieving at least $260 million of cost-out synergies this year, regardless of the macroeconomic environment, as most of these cost savings can be achieved internally. The market has been quite sceptical about the management’s ability to gain synergies from the merger and deliver 12% earnings per share growth in FY26, despite their vast experience in integrating global packaging businesses. This result shows that management’s plans are on track.

Portfolio Strategy: Amcor is the largest global packaging company with operations in 43 countries. While packaging is not the most exciting of industries, Amcor exposes its portfolio to global growth in consumer and medical goods, as well as manufacturer demands for increasingly sophisticated packaging. 95% of AMC’s customer base is in consumer staples, including packaging for meat, cheese, sauces, and condiments, as well as beverages, coffee, pet food, healthcare, and personal care products, all of which exhibit stable defensive characteristics. AMC looks extremely cheap in the context of the expensive ASX 200, with AMC trading on a PE of 10x with a full-year dividend yield of 6.7%.

AMC finished up +5% to $12.78

- Profits Up: First-quarter earnings per share increased by +18% to $687 million, with higher profit margins and synergy benefits from Berry offsetting a 2% decline in volume. Amcor management expects the business to return to growth over the coming year, following the Berry merger, as it can now manufacture more products at higher margins. (See Below)

{kind=link}